Why You Shouldn’t Underfund Your Brokerage Account

Recently, someone sent me a message saying they don’t want to contribute to their taxable brokerage account because of taxes. I get it, paying Uncle Sam fucking sucks.

So, I probed and asked why not? It’s an investment account where you can withdraw funds before age 59.5 without being penalized. She said, “I don’t want to be taxed on my money that I’m investing AND taxed upon withdrawal.”

Understood, SARAH.

But, let’s just say you earned $1,000 in capital gains by investing, and you had to pay 15% long term capital gains tax upon withdrawal. You would pay $150 in taxes, but you would have still earned $850.

Therefore, you would have $850 less if you didn’t invest at all in your taxable brokerage. So I asked, “Do you still not want to invest in a taxable brokerage?”

She said yes. So I threw my arms up, slammed my forehead on my desk, and figured I’d enlighten her about how there is actually a way to withdraw from your taxable brokerage and pay $0 to Uncle Sam.

Yes, it’s legal. And I’m going to get into it but I want to back up for a second and explain a bit about taxes paid in a taxable brokerage account.

Taxes, shmaxes.

No one likes ‘em, but we all gotta pay ‘em. Good thing tax optimization turns me on. But before I overexcite you, let’s chat about taxable brokerage taxation.

When purchasing securities (bonds, stocks, mutual funds any capital asset), you will either generate capital gains or losses depending on how much you paid for the asset, and how much you sell it for.

But, even if you don’t sell your stocks or bonds, you can still have taxable events within your brokerage account if you are paid dividends. Stocks pay dividends, and even if you automatically reinvest back into additional shares of that stock, you will still pay taxes. The same goes for money in your money market or high yield savings account. You pay taxes on the money you earn just as you do with your income. You’ll pay your ordinary tax rate for income on investments.

Quick example: If you earn $2,000 in interest and you are in the 24% income tax bracket, you’ll pay $480 in income tax on that interest. Simple enough, right?

What about capital gains tax?

Capital gains are generated from the buying and selling of capital assets, such as stocks, mutual funds, or ETFs. You’ll pay capital gains tax on qualified dividends and interest earned in your taxable brokerage account.

The good news: Capital gains tax rates are typically lower than ordinary income rates. In fact, they can be 0%. But first, let me break down short term capital gains tax and long term capital gains tax.

Short term capital gains tax is when you sell a capital asset after owning it for less than one year, which is taxed as ordinary income.

Long term capital gains tax is when you sell a capital asset after owning it for more than one year, which is then taxed anywhere from 0%-20%.

Understanding the distinction between both of these is important, because you want to avoid short term capital gains tax as much as possible so you can benefit from a reduced tax rate.

I realize I’m not encouraging you to fund your brokerage account after telling you about all of these taxes. BUT, I am getting there. Let’s start with me telling you all pros of a taxable brokerage account.

Taxable brokerage accounts are sexy because…

There are no income limits. Meaning, if you make $30,000 per year or $3.8 billion per year, or you’re Jeff Bezos, you can still invest in a taxable brokerage account. With a Roth IRA, phase out begins at $129k annually for singles and $204k annually for those married filing jointly. Phase out means you can no longer contribute the full $6,000 per year and would be contributing less per year.

There are no contribution limits. You can contribute as much money as you want. With a Roth IRA, you’re capped at $6,000 ($7,000 for age 50+) per year if you are under the income limit.

You can withdraw funds anytime without penalty. Unlike a 401(k) or IRA, you don’t have to wait until you’re 59.5 to to pay a 10% penalty for withdrawing funds before age 59.5.

There is a way to withdraw funds from a taxable brokerage account and pay $0 in taxes. YeS LeAnDrA, yOu’Ve mEnTiOnEd tHat FiVe TiMeS nOw.

Okay okay, I’m getting to it. Sheesh.

It all starts with long term capital gains rate. Remember when I mentioned that when you sell a capital asset after owning it for more than one year, you’ll be taxed anywhere from 0%-20%?

Good. Because the 0% was not a lie. Let me show you.

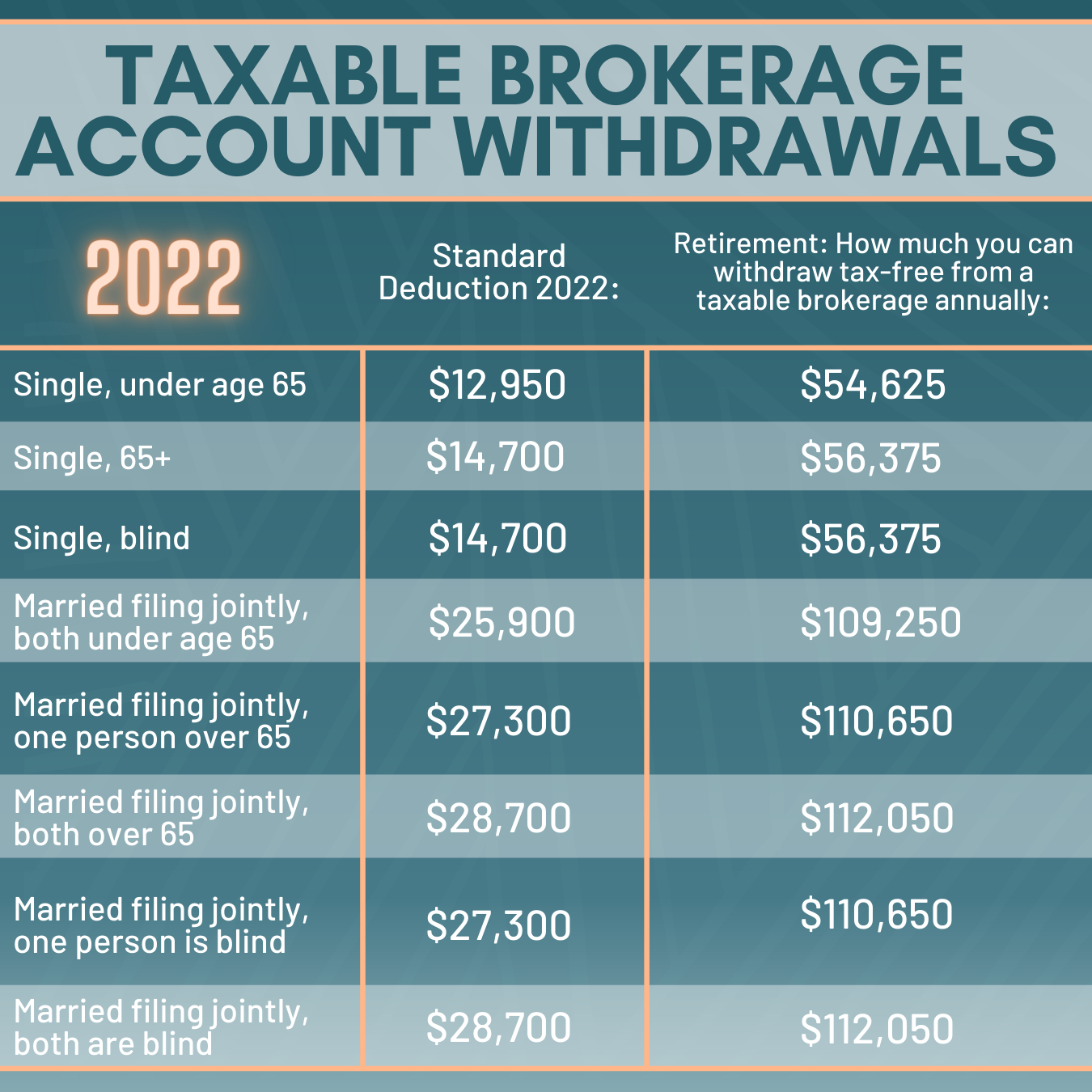

Assuming you are fully retired, these are the total amounts you could withdraw from your taxable brokerage at 0% in 2022. These numbers will likely increase each year to stay in line with inflation.

With a taxable brokerage account, if you are single and retired, you could withdraw $54,625 tax free before age 59.5. If you are married filing jointly, you could withdraw $109,250 tax free before age 59.5.

The maths:

Singles: Can withdraw $12,950 for the standard deduction + $41,675 is taxed at 0% long term capital gains rate.

Married: Can withdraw $25,900 for the standard deduction + $83,350 is taxed at 0% long term capital gains rate.

Here’s an example for anyone who is single and retired.

Ana is a single lady and has $1.4M in investments. She wants to live off of 4% of her investments, due to the 4% safe withdrawal rule. 4% of $1.4M is approximately $54,000, which is what Ana spends annually.

The maths:

The standard deduction for 2022 is $12,950). In addition, the exemption on the first $41,675 in capital gains for single filers is 0%. This means Ana can withdraw $54,625 TAX FREE!

If Ana needed to withdraw $60,000 per year, she would pay some capital gains tax when withdrawing from her brokerage account.

The first $54,625 would be taxed at 0% and the remaining $5,375 would be taxed at 15% which is $806.25 in taxes for the entire year. NOT BAD. Let’s look at it if you are married and file your taxes jointly.

Here’s an example if you are married and retired.

Stacy and her hubby have $2.7 million in investments. They plan to live off of 4% of their investments, due to the 4% safe withdrawal rule. 4% of $2.7 million is $108,000, which is what they will spend annually.

The maths:

The standard deduction for 2022 for married filing jointly is $25,900. In addition, the exemption on the first $83,350 in capital gains for those that are married filing jointly is 0%. This means they can withdraw up to $109,250 TAX FREE every year.

Let’s say they plan to withdraw $120,000 per year. They would pay some capital gains tax when withdrawing from their brokerage account.

The first $109,250 would be taxed at 0% and the remaining $10,750 would be taxed at 15% which is $1,612.50 in taxes for the entire year.

Retirement accounts are still important.

There are a lot of accounts when it comes to investing. I understand it can be confusing as far as how much to invest in each account, in what order, and for the best tax optimization. This is the typical order of operations I have for investing:

401(k) up to employer match only

Health Savings Account ($3,600/year)

Roth IRA ($6,000/year)

Invest back into your 401(k) and max it out (as long as the fees not more than 73 basis points higher than your taxable brokerage account)

Taxable Brokerage Account

This order does not take into account a Solo 401(k) or SEP IRA for those that are self employed.

And as far as #4, I have an explanation for this that I will save for another blog post. But, if your fees in a 401(k) are 73 basis points higher than a taxable brokerage account, then I would contribute to a taxable brokerage account instead of a 401(k).

The fees in my old 401(k) were 125 basis points higher than my taxable brokerage which is why I did not choose to max out my contributions, and instead funneled money into my taxable brokerage account.

Sarah, if you’re out there…

Please invest in a taxable brokerage and don’t be scared of the taxes in a taxable brokerage account. If you have any inclination of retiring before age 59.5, having funds in a taxable brokerage account is necessary to avoid paying penalties from your retirement accounts.

Moral of the story: Focus on your 401(k) and Roth IRA, but don’t underfund your brokerage account.

Cheers.